random cryptocurrency / cryptoeconomics thoughts #9

random cryptocurrency / cryptoeconomics thoughts #9

The below is unstructured, thinking out loud, a collection of thought bubbles written as a raw slab and is not factored for concision/to make it easy to read. There is not a sequential flow, paragraphs/ideas are random and undisciplined. No effort is made to stage them for easier reading/ingestion. The goal is to approach the synthesis / elaboration of fresh ideas and compounded concepts that ideally lead to further expanding the possible thinking around blockchain.

Blockchain Heresy:

The advance of intelligence is arguably measured as being the accumulating ledger/record of progress in a social grouping’s tolerance (and/or embrace) for its heretics, critics and infidels.

“The test of a first-rate intelligence is the ability to hold two opposed ideas in mind at the same time and still retain the ability to function.”

F. Scott Fitzgerald http://quoteparrot.com/quotes/f-scott-fitzgerald/127607-the-test-of-a

Blockchain natively entertains oxymorons such as ‘private blockchain’ and ‘stable coin’ and ‘on chain governance’ and ‘crypto investor’. [An example also of ‘cognitive dissonance’?] It seems to be endemic to blockchain that it throws up these face-off confrontations, where you have to be able to accommodate two logically-opposing notions yet somehow still find a way forward whilst pandering to both opposed sides. The cognitive load this requires may exceed the human mind’s native capacity (‘processing fluency’).

It may prove the case that the entire future viability of blockchain depends on our ability to tolerate this kind of ‘cognitive dissonance’, it seems native to the blockchain space. Heresy (embrace your heretics) may be an inherent requirement for progress and viability of blockchain (cryptopolitics/crypto-canon). It may be a requirement for all humans to live in sustained mode of ‘cognitive dissonance’ in order for blockchain (as a whole) to be live (progressing) and functioning. For example, we might always have to maintain both Bitcoin and Ethereum as equal-but-different primary replacements for the fiat US Dollar hegemony.

Human ingrouping (families, nations, unions) is normally a mechanism that does not easily tolerate heresy. Arguably, ingroups typically/usually function and arise so as to be a perimeter guard against heresy (strangers who threaten your gene/meme pool). Yet it may be the case that blockchain is exclusively none other than the summed total of its heresies — blockchain may always be a morass of conflicting ideas, waring sides, oxymorons, logical paradoxes (Byzantine General’s Problem — you can’t trust any of those in proximity): blockchain may always be composed of opposed forces that perpetually disagree or battle. 21st century society as a whole might have to learn that unless there are attendant heresies, then things aren’t right with our blockchain(s). This is not a normal way that most human minds function as [typically harmony-seeking] social members (given that ingroups repel their heretics) and will thus be a forever impost load on our cognitive capacity due to this.

It is not a lost irony that whilst the case may be that blockchain has always to be able to embrace heresy at the political/social/governance level, blockchains at a code/operational level eschew heresy: consensus mechanisms inherently are about forming consensus of a shared common ‘single’ truth record/ledger, thus explicitly not allowing parallel reality of the canonical chain = no ‘heretical’ blocks/chains. This of course sets up its own dissonance loading instance: heresy in our minds whilst there is finality in our chains.

Smarter minds in blockchain act to guard the notion that blockchain is not so much trustless as it is about trust minimisation. This is a fundamentally important notion about blockchain to grasp. By analogy, we might say that humans can not often identify truth, things that are absolutely true, but that we can/should instead hope for ‘high degree of truthiness’: things about which we can have high confidence, which hold in most cases, which have survived lots of test cases (Lindy), but which might fall down in certain edge/corner cases or which might be superseded one day by better theories/frameworks. Should you always trust that a canonical chain is always and forever true, immutable, fully trustworthy, fully true? Well, yes, a blockchain if a strong proof system, but…..

Sufficiently motivated governments and their NSA agency supercomputers are capable of amazing alternate realities. Should you instead rely on a canonical chain being a public ledger that reached highest consensus, was most true and most accepted by its diverse peer set? This is perhaps a reflection or outcome of human devices/works being always subject to the human capacity to ‘game the system’. Blockchains thus seek to be trust minimising systems rather than ‘absolute truths’ of unquestionable veracity. A blockchain’s ledger thus is the best recording system we have yet of a consensual agreement, but it is not an unassailable fortress; of course blockchains are the best answer we have ever yet arrived at, but perhaps they are not the last word and improvements might arise one day. As massive blockchain enthusiasts, we of course want to believe blockchain is the perfect system of record, the best record of truth we will ever have, but we need to be sober about the human capacity for cheating/gaming.

There is an oft-stated maxim that blockchain has yet “to find its killer app”, as if blockchain cannot possibly survive at all unless and until it finds some kind of all-conquering extra/supra use case that seven+ billion humans clamour to adopt in a gigantic rush. The implied sense is that the base, bottom chain/function is an insufficient entity on its own.

The risk here is for us all to succumb to the thought that we ought not invest any further into the existing blockchain movement unless and until some alien genius/white knight superbeing rides up and delivers us a brand new never-seen-before killer app that makes us all goggle with wonderment.

The cost of this waiting room mentality is lost opportunity cost. If we think current blockchain is insufficient, the risk is that for some time to come, whilst we hover in a cautious holding pattern, that we hold back and refuse to take risks, because we think a saviour will appear soon and deprecate our sunk time.

The killer app of blockchain is blockchain: no superior use case will ever emerge. Doubtless, new apps will arise one day that add much extra, fresh, unique value on top of base chains. Should we wait forlornly until then, idle ourselves and stay modest in our risk taking? Is the blockchain base case invalid until some future superbeing bequeaths us some godly heretofore-unseen killer app?

Markets (bonds, forex, options, etc.) are well-recognised economic constructs. The obvious intuition is that markets exist to allow/ensure the emergent property of optimal resource allocation occurs — markets magically ‘figure out’ where to allocate resources in the best (socially optimal) way, as indicated by the price a market is traded at.

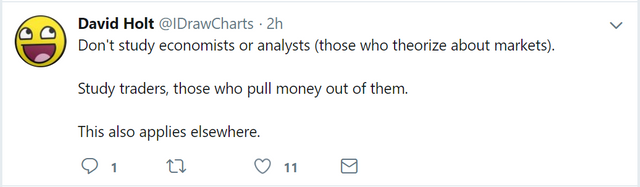

https://twitter.com/IDrawCharts/status/1112864240354906112

A crypto-influenced view may instead posit that (crypto-specific) markets exist as mechanisms that incent ‘hackers’ (i.e. traders) to exploit them/probe them (each coin project, e.g. BTC, ETH) so as to find their fault lines and thus criticise/collapse them. In this sense, crypto-market traders are explicitly incentivised to ‘hack away’ (i.e. make trades) as (perhaps unknowing) penetration testers (ethical hackers, white hats) of the underlying social rationale for a given crypto project’s existence.

Whereas traders of ‘traditional’ equities -such as AAPL (Apple stock) — are incentivised (e.g. by buying APPL) to share in Apple’s future cash flows as a company that seeks to produce profits for shareholders, crypto-traders instead profit if they best unlock the global social value of the weakness or strength of the crypto meme itself. Crypto-traders in this sense ‘decide’ if a coin deserves to survive by buying it/HODLing or by selling out of it and buying an alternate (stronger, more fit to survive) project’s coin. Crypto-traders can ‘overload’ a coin if they wish to hasten its demise (the CryptoKitties overload event in late 2017 that threatened to crash the massed ethereum nodes/miners). Traders of crypto markets are in this sense incentivised to figure out which cryptocoin is strongest/best deserves to thrive (is hardest to hack/short into nothingness), more so than traditional traders are asked/paid to determine the underlying relevance and deservedness of their markets and the individual fitness-to-survive of the issuances involved. Traders of AAPL shares are not (in the large part) paid for their opinion of AAPL’s right to exist, whereas buying Ether is inherently a statement of belief in Ethereum’s future and codebase soundness.

Cryptoeconomics in this sense encourages its markets to work not for classical ‘price discovery’ reasons but more so for cryptoeconomical ‘attack surface discovery’. Crypto-markets incent traders to find the weakness in the crypto-marketplace or a given coin. Crypto-markets reward those traders (hackers) who best either a) identify then exploit that weakness or b) furnish the coinz’ soundness.

Just as George Soros famously shorted the British £ Pound Sterling in the early 1990’s as his way or criticising the Bank Of England, so too do crypto-traders seek for exploits via the traded price/markets of cryptocoinz and the coinz’ inherent cryptoeconomics — if the coinz’ cryptoeconomics is weak or has fault lines, then crypto-traders are primarily rewarded for finding-then-exploiting them. This is why we have seen 51% attacks against coinz/projects such as Bitcoin Gold, Ethereum Classic. Blockchain wants you to find its weakness, crypto-traders and crypto-markets are a source of hackers for this effort. Traditional markets have regulators and police to protect them from hackers; crypto markets actively pay their participants to find their weaknesses.

Disclaimers:. YMMV. This is not investment advice. I’m ego-driven, clueless and biased, so do your own thinking. I’m not qualified, I have no special privileged position to drive my insight, I’m a nobody, is what you should assume about me and what I say here.