This Thing Called Blockchain… [Beginners Guide]

This Thing Called Blockchain… [Beginners Guide]

Introduction

My friends and family members knowing my educational background and passion for new technologies, frequently ask: what is this blockchain anyway, is it true I can make some money on it?

After many such situations, I decided to write this article, which I hope will be digestible even by the less technically inclined ones.

Without a doubt, blockchain technology definitely brought a fresh intake of new ideas in various spheres of our lives. Apart from ideas, its solutions also have an aim to revolutionize not the just the global financial system but business conduction as well.

Thus, this review about blockchain to clear misunderstandings regarding its network, ledger records, innovativeness, and future outlook. For those interested in ICOs and purchase of cryptocurrencies, head over my other articles that cover these topics.

Disrupting technology

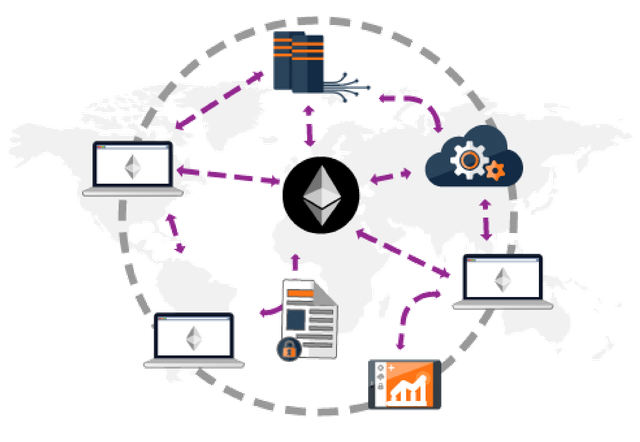

The blockchain is a new technology that provides (almost) free-for-all ledger records of all transactions within its boundaries. It is also a transfer system in which parties can send, receive, and keep digital coins for a variety of reasons. Thus, it is important to understand that cryptocurrencies are just sphere of the blockchain, which holds a lot more applications in the real world, not just holding coins of value. Apart from transactions, any sort of information can be recorded. Any of the records cannot be changed on the latter date, as to provide complete transparency.

The main goal of blockchain technology is to provide a completely decentralized environment, where participants of the system create and maintain the network. The database is equally available to all individuals, regardless of their background and wealth.

Since its establishment in 2009, there have been a variety of blockchain systems up to date. Some systems allow mining and transfer confirmations, as a self-regulated approach to financial issues (bitcoins), while others offer smart contracts as a fail-free way to conduct instant business for low fees (Ethereum).

Innovation in Blockchain

As mentioned before, the blockchain technology went a long way to establish its base in financial systems around the world. Through ICOs (Initial Coin Offerings) and companies that develop the said network, a lot of interesting projects were established in recent years.

Take Ethereum for example. Prior to the project in 2017, bitcoin lead the way with its mining confirmations, in which several miners needed to pick up transactions and confirm them through hash power. Ethereum introduced smart contracts, which were online agreements between two or more parties regarding transfers. The transfer would keep all agreed upon points, where value, timing, and content of agreement would be automatically carried out.

Source: News Bitcoin

Next step was a lightning network, introduced by Joseph Poon and Thaddeus Dryja in 2015, which was developed as a solution to bitcoin’s scalability issues. It is placed on top of the blockchain’s network, where transactions would connect peers without confirmations, increasing the transfer speed and security. The whole system is based on microtransactions, where multiple parties can form without the use of blockchain’s transfer system and yet be kept in ledger records.

We now have many other systems that solve several issues, such as Ripple (banking system), Monero (fungibility and decentralization), Dash (nods instead of centralized supply), Cardano (decentralized development), and many others as well.

Application in Various Industries

The blockchain is not meant to be worlds apart from common business industries. On the contrary, many of these systems aim to fix issues that the current system faces, in terms of centralization, monopoly, the speed of information & fund transfers, and transparency.

Through smart contracts, for example, Ethereum and other projects aim to provide a safe ground where the middle party would not be needed. The cost of transferring value from one side to another would thus be lowered significantly, while transfer speed would surpass banking services by far.

Bitcoin and all other cryptos can be used as a medium for payment for goods and services. Thus, using crypto retail, pharmaceutical, and other industries would experience a decentralized yet unified marketplace, where participants from all over the world can purchase and sell their services without boundaries.

Scams and Hacks

Although innovative, blockchain is also prone to be misused, as with anything else in the world. There have been many platforms that offered too-good-to-be-true systems for investors to dive in, especially through ICOs.

Famous examples of such scams are Pincoin and iFan, both of which brought in $660 million worth of investments. Companies behind these projects promised lightning-fast transactions, secure transfer system, and privacy, only to take the money and disappear without a trace.

Hacking attempts in the past also proved the point that current blockchain networks needed better solutions in terms of safety. Bitfinex ($72 million) and Mt. Gox ($473 million) give out a warning sign that ledger records, although providing transparency, cannot stop the theft of assets, even if address codes are revealed.

Coins and Tokens

As a result of blockchains, tokens, and coins came to life. Currently, there are over 1.000 cryptocurrencies that signify the same amount of blockchain n networks in the world. These tokens are used as a medium for payment and value transfer within their own systems and are used to transfer value from all corners of the world.

Some are minable and some are not, depending on the developer’s idea on how blockchain world should be organized. These cryptocurrencies can be evaluated through fiats or through services they provide for participants.

What About Mining?

There are two ways on how tokens would be distributed within the blockchain’s system. The first is through mining, which bitcoin, Ethereum, Litecoin and many others use. Individual participants would provide their computer’s hash rate and mine cryptocurrencies in order to be awarded blocks. Then, they would sell them out and earn profits from their operations while the market is supplied by the amount awarded by the blockchain.

Others, like Ripple, IOTA, and Cardano, monopolize the supply as to avoid rapid fluctuations in value. Developers keep the supply to either control the price as their blockchain systems are meant for purposes other than trading and mining. In these systems, participants would usually purchase coins in order to use them for online services.

Conclusion

All in all, blockchain provides promising solutions to issues that our financial systems and other industries currently face. However, there is also lots of room for improvement, signifying the need for innovation especially in the crypto world.

Luckily, we have many exciting projects planned for in 2018 and 2019 and judging from the number of cryptos currently in the market, the blockchain networks are yet to show what they can really do.