Will U.S. Treasury Yields Go Negative?

The relatively high and positive yields in U.S. government bonds have been an outlier in global markets, but coronavirus blowback appears on track to wipe away that spread (or at least make a hefty dent). Rates are still positive across the Treasury curve in early trading on Friday (Mar. 6), but downside momentum rolls on and as the global risk-off trade accelerates the prospect of below-zero yields in U.S. is becoming increasingly plausible at some point in the near future.

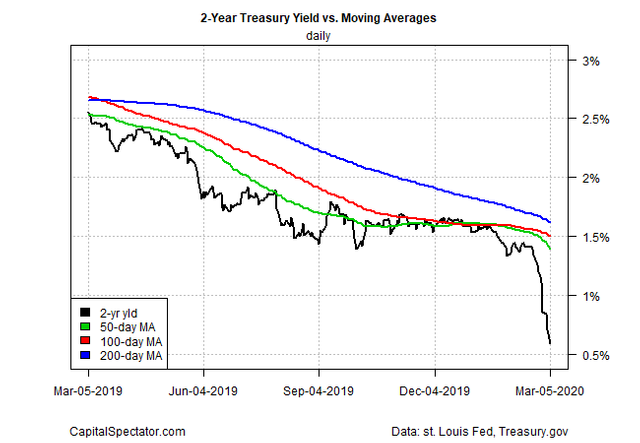

If recent events are a guide, the short end of the curve could go negative within days or weeks. Consider the 2-year Treasury yield, which has fallen sharply this week. This maturity, which is widely seen as the most sensitive spot on the curve for policy expectations, fell to 0.59% yesterday (Mar. 5), based on daily data via Treasury.gov. That’s the lowest since 2014.

2 Year Treasury Yield Vs Moving Averages Daily Chart  2 Year Treasury Yield Vs Moving Averages Daily Chart

2 Year Treasury Yield Vs Moving Averages Daily Chart

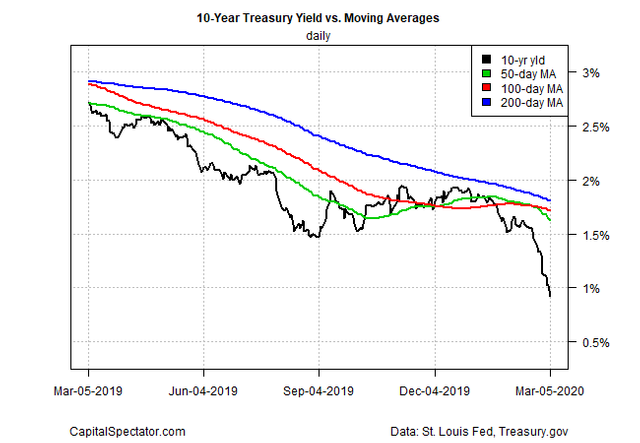

The benchmark 10-year yield is also dropping like a stone and tumbled below 1.0% on Thursday for the first time. 10 Year Treasury Yield Vs Moving Averages Daily Chart  10 Year Treasury Yield Vs Moving Averages Daily Chart

10 Year Treasury Yield Vs Moving Averages Daily Chart

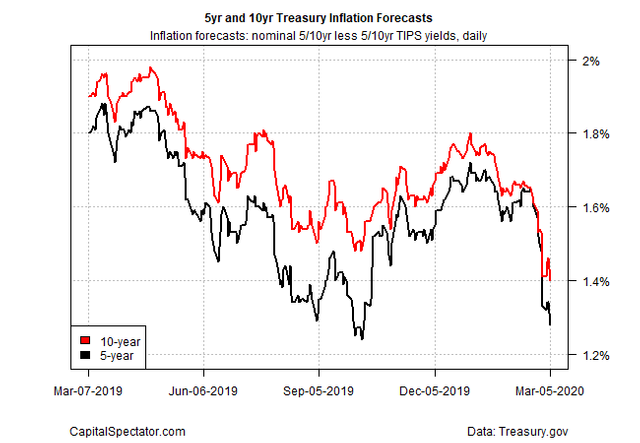

Inflation expectation are also sliding. The implied forecast via the spread on the nominal 5-year Treasury less its inflation-indexed counterpart dropped to 1.28% on Thursday (Mar. 5)—far below the Federal Reserve’s 2.0% inflation target and the 2%-plus annual rise in consumer inflation reported for January. 5 Yr And 10 Yr Treasury Inflation Forecasts  5 Yr And 10 Yr Treasury Inflation Forecasts

5 Yr And 10 Yr Treasury Inflation Forecasts

Some analysts are looking at the Fed’s latest emergency 50-basis-point cut as a sign of more easing to come. “If we look at history, once the Fed does a panic, inter-meeting rate cut, particularly when it’s 50 basis points … they typically cut pretty quickly again,” says Double

Line Capital CEO Jeffrey Gundlach. “I’m in the camp that the Fed is going to cut rates again, perhaps even in two weeks” at the March 18 meeting.

Fed funds futures are pricing in high odds of another rate cut in two weeks. As of early trading today (Mar. 6), the crowd’s estimating a virtual near certainty of additional easing later this month, based on CME data.

Pressure for rate cuts is coming from multiple sources, including a global selloff in risk assets linked to fears over the spreading coronavirus. “Markets are struggling to balance the competing forces of more extensive virus containment measures, and of monetary and fiscal stimulus,” says Mark Haefele, chief investment officer of UBS Global Wealth Management.

For bond markets, the path of least resistance for yields is down as demand surges for safe havens. For the moment, the dive in rates appears to be triggered by sentiment rather hard economic data. ADP’s estimate of US private payrolls for February, for instance, posted a healthy gain.

Meanwhile, recent nowcasts for GDP in the upcoming first-quarter report continue to anticipate that the expansion will roll on. The Atlanta Fed’s GDPNow model, for instance, estimates output will rise 2.7% in Q1 (as of Mar. 2), above Q4’s 2.1% increase.

The question, of course, is how much coronavirus blowback is lurking? Incoming data in the weeks and months ahead will suffer in some degree. The degree of the suffering is unclear at this point, but investors are running for cover now and asking questions later.

“Zero percent yields are no barrier to any bond market in the developed world right now,” advises Shaun Roache, chief Asia-Pacific economist at S&P Global (NYSE:SPGI) Ratings. “It’s an insane market — investors are re-defining the idea of risk distribution.”

Hi! I am a robot. I just upvoted you! I found similar content that readers might be interested in:

https://www.capitalspectator.com/will-us-treasury-yields-go-negative/