SLC | S21W6 | Costs for entrepreneurs - Cost structure

What is a cost structure, and what is its importance for the business?

A cost structure is the set of principles and methods used to identify, organize and classify all costs related to the operation of a business, it includes fixed costs, such as rent, salaries and machinery depreciation, which remain constant regardless of the level of production and variable costs, such as the materials necessary for production or energy consumption, which fluctuate depending on the volume of activity. This structure is not only limited to listing expenses but classifies them according to their impact and direct or indirect relationship with the offered products or services.

In the context of entrepreneurship, the cost structure is a key component for the financial management and long-term success of the business, it allows you to identify areas of expense and optimize the use of available resources which helps improve operational efficiency. It also provides a solid basis for informed decision making by allowing accurate calculation of sales prices, profit margins and expansion or adjustment strategies. Additionally, it acts as a financial control tool, helping entrepreneurs to forecast and mitigate potential problems before they seriously affect the sustainability of the business.

For example, in a company that makes artisanal products, such as candles, the cost structure would include workshop rent and salaries as fixed costs, while materials such as wax, fragrances and wicks would be variable costs, this detailed breakdown allows the entrepreneur to understand how expenses are distributed and where they can save or invest to improve profitability, a well-designed cost structure also allows entrepreneurs to be more competitive, either by reducing costs to offer lower prices or by investing in quality to justify higher prices, It also facilitates long-term planning by establishing realistic financial goals based on the analysis of current and projected costs.

Provide examples of businesses that use the cost structure methods explained; explain your answers.

Take the case of my country Tunisia, companies adapt their cost structures according to local market realities and consumer expectations, take the example of supermarket chains such as Monoprix and Carrefour Tunisie, these brands adopt a cost structure focused on reducing expenses to offer products at competitive prices, they optimize their supply chains by working with local and international suppliers at advantageous prices, moreover, they increase their margins by offering premium brands distributor, which cost less to produce while ensuring acceptable quality.

In the fashion sector, companies like Hamadi Abid position themselves with a value-oriented cost structure, this Tunisian brand, well known for its clothing, invests in premium materials and manufacturing processes which guarantee careful finishes, it targets a local and international clientele who are ready to pay more for elegant and durable products, the strategy is based on the creation of a strong brand identity and on the highlighting of quality as an element differentiator, which justifies prices higher higher compared to other local brands.

In the fast food sector, local chains like baguette et baguette combine these two approaches by offering affordable products, while adding value through customization and quality of ingredients, although the prices are competitive , customers appreciate the generous portions and traditional recipes adapted to local tastes, this hybrid approach attracts a diverse clientele, from students to families, while maintaining an image of quality and proximity.

Source

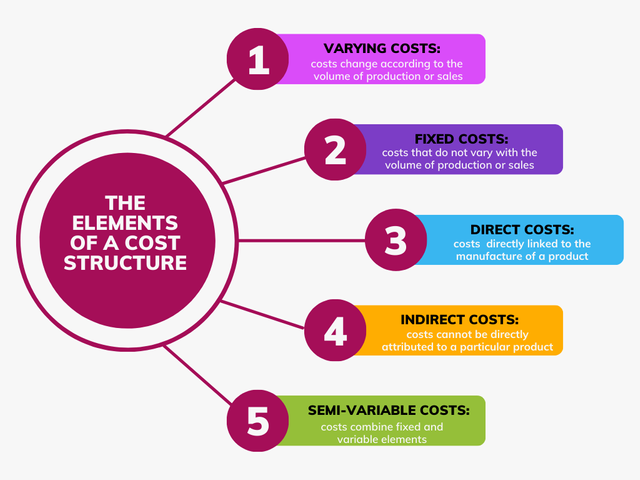

What are the elements of a cost structure? Provide examples.

The elements of a cost structure are the different categories of expenses necessary to operate a business, these elements are generally classified according to their nature and their relationship with the product or service offered, understanding these elements is essential to analyze the finances of a company and make strategic decisions.

Varying costs:

These costs change according to the volume of production or sales, they increase when activity increases and decrease when it slows down, in a Tunisian textile factory, the cost of raw materials such as cotton or fabric is an example of variable cost, since it directly depends on the quantity of clothing produced, another example is the energy consumption used by the machines during production.

Fixed costs:

These are the costs that do not vary with the volume of production or sales. They remain constant, whether a company produces a lot or a little, in Tunisia, a typical example would be the rent of a commercial premises. A bakery, for example, will pay the same amount of rent each month regardless of the quantity of bread produced, similarly, the salaries of full-time employees are a fixed cost.

Direct costs:

They are directly linked to the manufacture of a product or the provision of a service, in a pastry shop, for example, ingredients such as flour, sugar, and eggs are direct costs, because they are necessary for the cake production These costs are easy to attribute to a specific product.

Indirect costs:

They cannot be directly attributed to a particular product or service, but they are essential to the smooth running of the business, for example, administrative costs in a Tunisian business, such as accounting or marketing services, fall into this category . Similarly, electricity used for lighting or air conditioning of the premises is an indirect cost.

Semi-variable costs:

These costs combine fixed and variable elements, for example, in a call center in Tunisia, part of the telecommunication costs could be fixed (a monthly subscription) and another variable part (the cost per additional minute depending on the 'usage).

Prepare the cost structure of a business dedicated to the production of cakes. It has a production of 5 cakes per day and expects to obtain a total profit margin of 25%.

To prepare the cost structure for a cake production business with a daily output of 5 cakes and an expected profit margin of 25%, we will calculate the costs and selling price step by step, taking into account both direct and indirect costs.

Step 1: Direct Costs per Cake

Direct costs are the expenses directly tied to producing each cake, such as ingredients. Assume the following breakdown:

| Ingredient | Cost per Unit | Quantity per Cake | Cost per Cake ($) |

|---|---|---|---|

| Flour (kg) | 2.00 | 0.5 | 1.00 |

| Sugar (kg) | 1.50 | 0.3 | 0.45 |

| Eggs (dozen) | 3.60 | 0.25 | 0.90 |

| Butter (kg) | 5.00 | 0.2 | 1.00 |

| Milk (liter) | 1.20 | 0.1 | 0.12 |

| Other ingredients | - | - | 0.50 |

| Total Direct Cost | - | - | 4.97 |

Step 2: Indirect Costs

Indirect costs include fixed and variable expenses that are not directly tied to individual cakes but are necessary for operations. Assume the following monthly costs:

| Expense | Monthly Cost ($) | Daily Cost ($) | Cost per Cake ($) |

|---|---|---|---|

| Rent | 300.00 | 10.00 | 2.00 |

| Utilities | 90.00 | 3.00 | 0.60 |

| Salaries | 600.00 | 20.00 | 4.00 |

| Maintenance | 60.00 | 2.00 | 0.40 |

| Marketing | 50.00 | 1.67 | 0.33 |

| Total Indirect Cost | - | 36.67 | 7.33 |

.png)

Step 3: Total Cost per Cake

The total cost per cake is the sum of the direct and indirect costs:

Total Cost per Cake = Direct Cost per Cake + Indirect Cost per Cake

Total Cost per Cake = 4.97 + 7.33 = 12.30

Step 4: Selling Price with 25% Profit Margin

To achieve a profit margin of 25%, the selling price is calculated as:

Selling Price per Cake =Total Cost per Cake *(1 + Profit Margin)

Selling Price per Cake} = 12.30 * 1.25 = 15.38

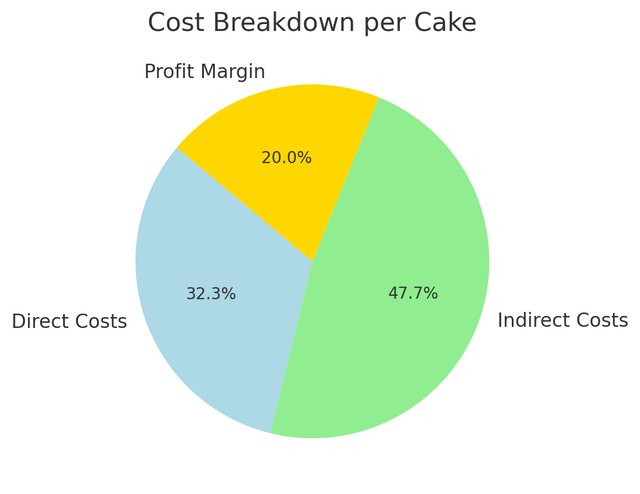

Step 5: Summary of the Cost Structure

| Category | Cost per Cake ($) |

|---|---|

| Direct Costs | 4.97 |

| Indirect Costs | 7.33 |

| Total Costs | 12.30 |

| Selling Price | 15.38 |

To meet the business's profit goals, each cake should be sold at $15.38. This ensures the business covers all its costs and achieves a profit margin of 25%.

Thank you very much for reading, it's time to invite my friends @sahar78, @stream4u, @fombae to participate in this contest.

Best Regards,

@kouba01

Assalamu alaikum!

I am happy to see that how beautifully you have explained costs for entrepreneurs. Especially it was a good thing to see that how you have described in summary in a graph about costs in which indirect cost have wide area.

I wish a lot of success to you......

You have shared a very nice and detailed post. You also add 5 elements of the cost structure that allow the entrepreneur to be able to implement this method in a specific way.

I admire your insight on this topic

Success is always for you.

Greetings @kouba01

1.- You have shared the concept and importance of the cost structure for the company, highlighting that it allows to control the resources invested in a productive process.

2.- You have mentioned acceptable examples of companies that conform to cost structure methods. You have provided the description of each of these methods, allowing the analysis of all the costs involved.

3.- You have presented the elements of the cost structure, with their respective examples; these allow us to identify the expenses in each functional area of the company.

4.- You have developed the proposed exercise acceptably, performing in detail each one of the calculations; besides you have presented the graphical behavior of the same.

Thanks for joining the contest