Gods of the Valley — Part 2: Google — The All Knowing Alphabet

We are entering into an era of unparalleled tech dominance. Companies like Google, Amazon, Facebook and Apple control more and more of our everyday lives — owning our data and everything around it. The inherent network effects and flywheels these companies built are unprecedented — both in their scope and ability to stave off competition.

This is the second in a series of articles breaking down not just the strengths and weaknesses of today’s top companies, but also speculating on future opportunities and acquisitions to help startups and investors plan accordingly.

Previously we dove into Amazon and came away with some pretty interesting conclusions and future predictions. Think Amazon will be the 1st trillion dollar company? I recommend checking out this article.

Google is god

In 1998 the world changed forever when two crazy nerds in a garage rewrote our idea of the internet. What was once a disorganized mess of information suddenly had structure — imagine a library without a filing system. That was more or less the state of affairs.

Google revolutionized search, bringing reputation based ranking to the results. And while the algorithm was anything but perfect, the network effects and perpetual tweaks continuously improved the results, resulting in the internet of today.

Now you ask Google (ie god) a question, and you get an answer. It is your go to source for information and one of the few universally recognized words (and verbs).

Just Google it.Understanding Google

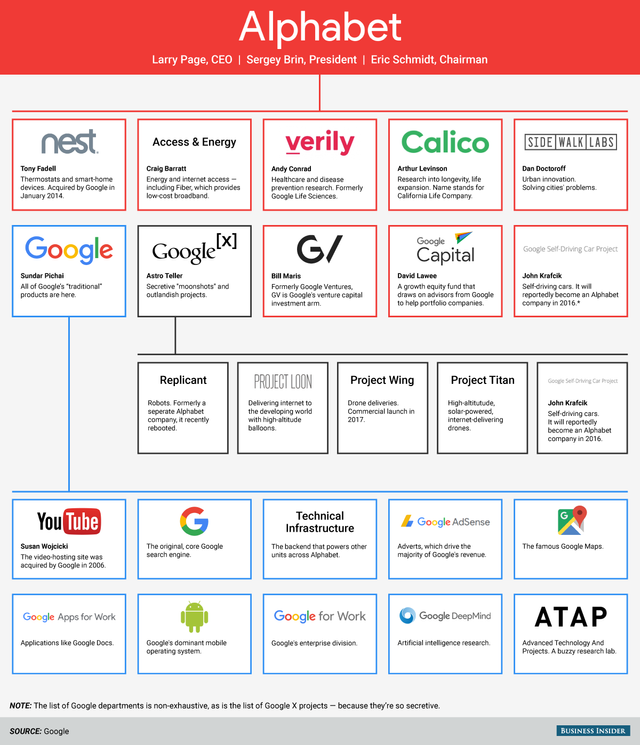

To understand Google and see where the company is headed, it is important to understand the constantly morphing and expanding organizational structure.

In 2015, Google officially became Alphabet, an overarching entity to let the many business units move faster and more freely to speed innovation.

And of any company today, Google is one of the most complex. These various entities are broadly divided into the (1) Core Google Products (the “Alpha Bets”), and (2) “Other Bets”.

The big Alphas include

While a bit further removed from the core of Google’s product, the Other Bets include an impressive range including: It is a mouthful. For a company focused on search, they sure do a lot. Don’t worry, we will breakdown each of the core areas to paint a better picture.

1. Alpha Bets — Google’s core

At its heart, Google is an information company. What started as a mission to catalog the world’s information has over time expanded to include in essence, owning the internet. Google’s various products are all focused on owning user attention — most of which is monetized via advertising.

Search — #1 search engine

Google is the dominant search engine. 77% of global searches go through Google (Source: NetMarketShare.com). Take a moment to let that number sink in.

Despite the fact that 1.3B people (there are only 7.6B people globally) live behind China’s Firewall, Google still owns over ¾ of the search engine market. This dominance has fueled Google’s historic rise.

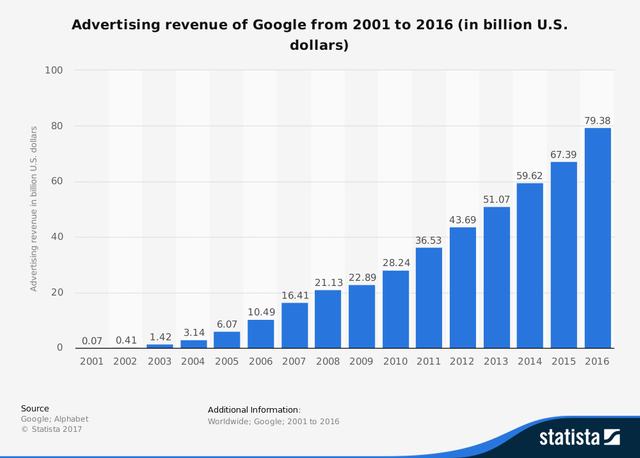

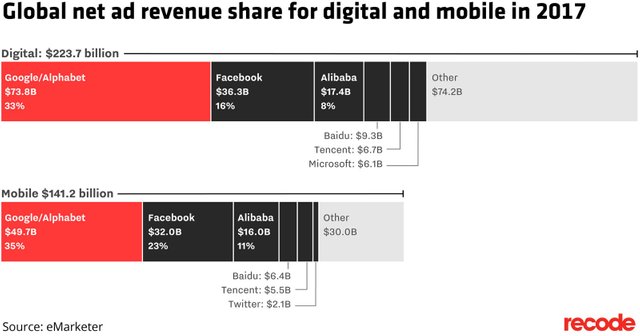

This power is problematic though. 86.5% of Alphabet’s revenue comes from advertising, primarily search ads (Source: Statista). Of course Youtube and Gmail ads plus AdSense make up a portion, but the lionshare comes from search ads.

Talk about all your eggs in one basket… we’ll continue this thread later.

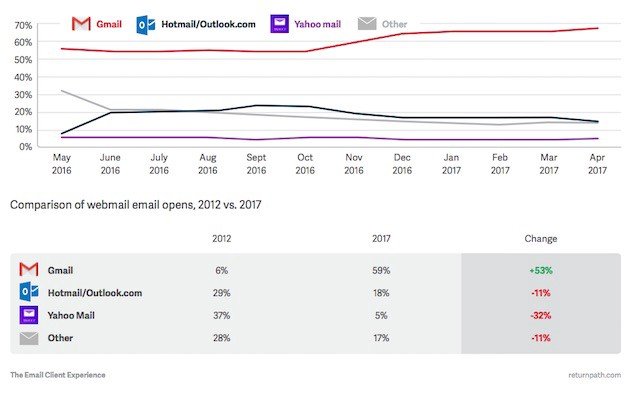

Gmail — #1 email service

If you’re reading this, you are probably a business person or techie. Either way you understand the importance of email (unfortunately).

While exact stats are sketchy (ability to own multiple emails), studies show that 60% of users use Gmail as their primary email. And while Google is clearly the dominant email service provider, this isn’t a big revenue driver for the company (especially after both infrastructure and employee costs).

And honestly, when was the last time you clicked an ad in Gmail.

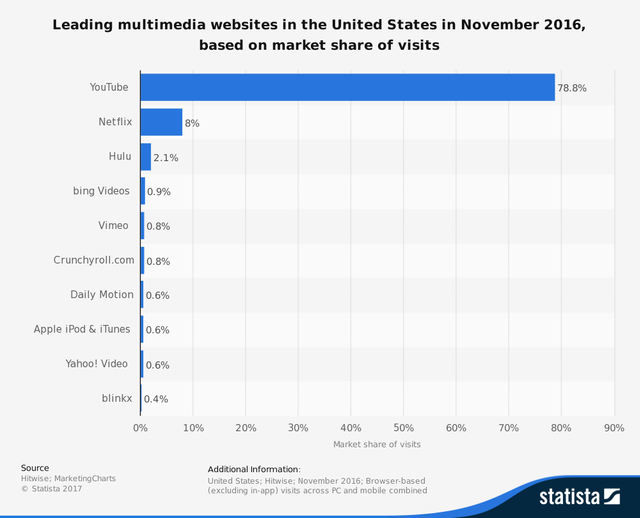

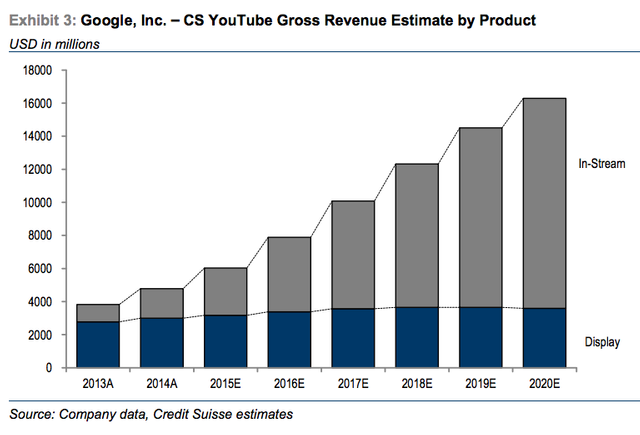

Youtube — #1 video platform

Youtube is the second largest search engine in the world, and easily the largest user generated video platform. Users upload an impossible 100 hours of content to Youtube every minute.

Considering Google only paid $1.65B to acquire them in 2006, that is one hell of a deal.

And while specific stats on Youtube’s contribution to the bottomline are not publicly available, Credit Suisse believes that in 2015, Youtube and Google Play accounted for ~15% of Google’s revenue (up from 4% in 2010), and forecasted to reach 24% by 2020.

Google Chrome — #1 internet browser

Chrome is far and away the most successful internet browser, owning over 60% of the world’s web browser market. And while Chrome doesn’t generate revenue, it generates mountains of data — and saves Google a fortune.

In 2013 Mozilla brought in $314M, 97% of which came from advertising royalties (setting Google as default browser). With between 5–15% of the global market (depending on source), this means Chrome’s 60% market share would save Google ~1.3-$3.8B/yr (assuming Mozilla’s royalty fees are roughly the same as other browsers). As market leaders traditionally warrant high multiples, this means Google Chrome’s division would be a massive standalone company on its own, without even taking into account the data value.

Google Maps — #1 maps program

While not technically a revenue generating part of Google’s business, Maps makes up a core piece of Google’s ecosystem and is incredibly valuable.

Advertising is a game of data, the more data (especially locational data) a company has, the better the their targeting. Remember, Google wants to own the internet and customer attention.

And while iPhone users are traditionally incredibly loyal to Apple (often to their detriment), studies show that 70%+ of iPhone users prefer Google Maps to Apple Maps. (Consumer Hardware’s a Horrible Business Model, So Apple Slows Down Your iPhone)

Google is now also experimenting with new ways of monetizing Maps, both with book an Uber buttons and likely many future locational advertisements as well.

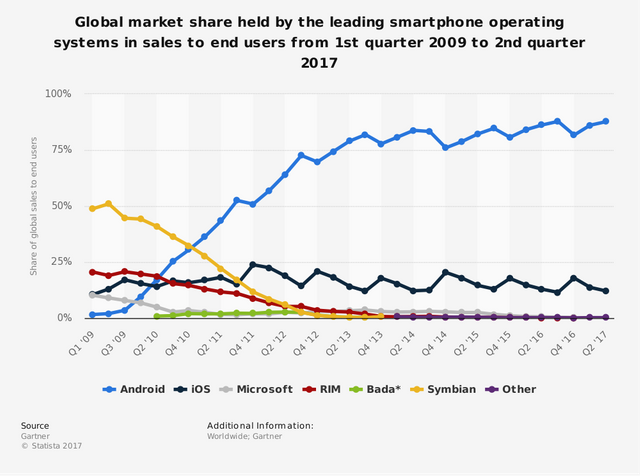

Android and Google Play — #1 mobile OS

In 2005 Google quietly acquired Android for a reported (unverified) $50M. What seemed at the time a foolish, overpriced bet has paid for itself hundreds of times over.

This acquisition served two primary purposes: saving money (realized later) and potential future growth.

In 2007 Steve Jobs introduced the iPhone. After this the world changed. And because Apple OWNED the smartphone market, Google got hit with the Apple tax. Basically Apple charged Google a percentage of iPhone ad revenues to let Google be the default search engine — costing Google a fortune in lost mobile revenue.

(NOTE: Today Google paid Apple $3B to be default iPhone browser, imagine if Apple owned the entire market…)

Android changed the game. Now 80–88% of phones sold every quarter are Android. Let’s face it, iPhones are too expensive for the worldwide mass market.

Thanks to this foresight and dedication to the Android ecosystem, Google leads mobile ad revenues with 35% of the market worldwide ($49.7B).

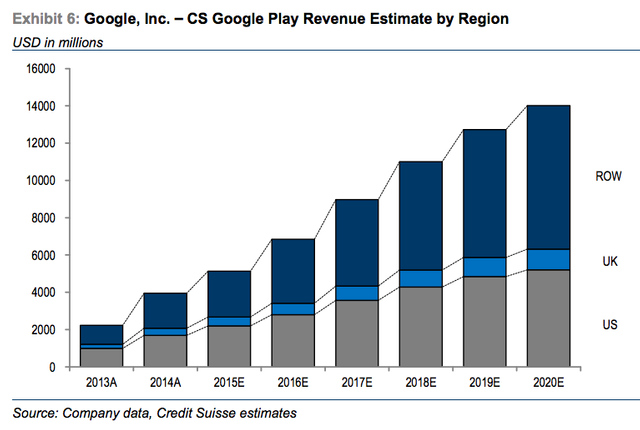

And that is without even addressing the app store, Google Play. Google’s 3rd party developer ecosystem is thriving, adding approximately $9B to Alphabet’s 2017 bottomline.

AdSense — #1 display advertising network

The other piece of Google’s advertising supremacy is their partner network, AdSense. AdSense allows sites to monetize through Google’s advertising platform without worrying about the backend or finding advertisers. Instead Google handles everything and takes a between 32 and 49 percent of ad revenue generate (the rest going to publishers).

According to Investopedia, AdSense revenues accounted for $15.5B, ie 23% of Google’s total revenue in 2016.

Unfortunately advertising as a business focuses on eyeballs over quality, leading to much of the degradation and click baity titles of today. I don’t see the advertising model changing drastically anytime soon, meaning Google’s great success with AdSense is likely to continue (and grow).

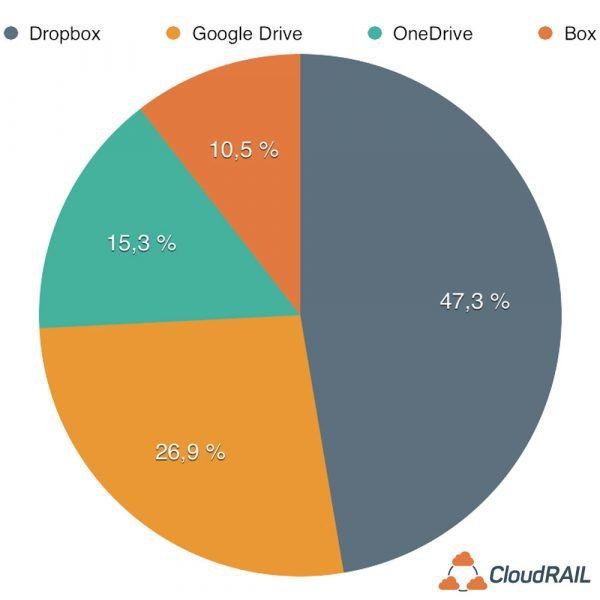

Google Drive — #2 cloud storage service

In 2012, Google decided they needed to compete with Dropbox and Box. The cloud storage market was taking off and Google (the best possibly positioned company for this space) was late to the game.

Today only Dropbox has a larger share of the market. And while cloud storage fees are relatively low, $1.99/mo for 100GB, those add up as more and more users backup everything online.

And the big value add is Google Docs. Online, editable documents and folders allow individual and teams to store and edit everything in the cloud. I have spilled enough cups of coffee to understand the importance of a backup.

While less dominant with today’s corporations, studies show that:

“When students write papers by themselves, only 12 percent use Google Docs. But when students write papers in groups — when they collaborate — 78 percent use Google Docs. On the other hand, 80 percent of students use Microsoft Word for individual work, and 13 percent use it for group work.” Recode

As more and more millenials enter the workforce, expect this trend to intensify as more individuals and organizations take to Google’s Cloud for ALL their documents and collaboration (providing a potentially lucrative growth opportunity for the company).

Source: SkyHighNetwork

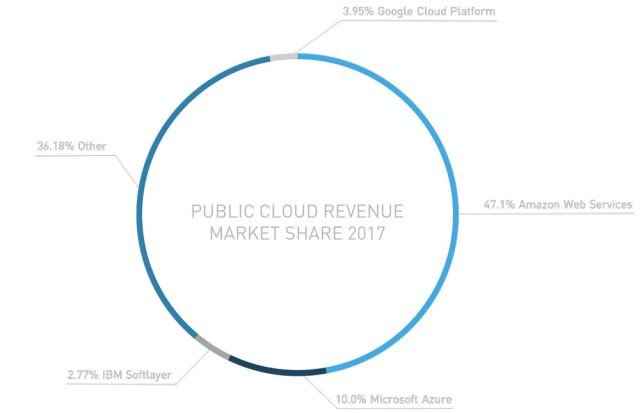

Google is also rapidly expanding their B2B Cloud infrastructure, but with only 3.95% of the market, they have a long way to go to catch Amazon — creating massive growth potential in this $25B+ market for IaaS (infrastructure as a service).

Source: SkyHighNetwork

DeepMind

Google bought DeepMind, a London based AI research lab in 2014 for a reported $500M. While the division doesn’t seem to bring in revenue, artificial intelligence is one of Google’s strongest and most defensible moats— making this a smart acquisition with huge potential ramifications for Google’s future success.

2. Other Bets

Google makes so much money, they don’t know what to do with all of it. That said, they are also justifiably worried about the state of their advertising monopoly. Voice based search errodes much of the conventional search market, meaning Google could be in trouble.

All of these divisions are focused on future growth and innovation and likely hold many of the keys to Google’s future dominance.

Waymo

In 2016 Google spun Waymo, their self-driving car initiative, into a standalone company. Widely recognized as one of the leaders in autonomous driving, Waymo could be the big win Google needs.

Waymo is currently suing Uber (another of the top contenders) for $2.6B in damages related to IP theft.

This is very relevant given the race for the OS (operating system) of autonomous vehicles will likely be a winner take all (or most) scenario.

Google Ventures & CapitalG

The other great thing about having a war chest is the ability to bet on the future. Google Ventures (GV) is Google’s venture capital arm (a $2.4B fund), focused on investing in the disruptive and gamechanging companies of the future — buying exposure to fast growing industries.

To date their portfolio is top notch, including the likes of Uber, Medium, Jet.com, Slack, Stripe, HubSpot and dozens of other promising startups.

GV not only presents great opportunities for future partnership and/or acquisitions (like in the case of Nest), but diversifies Google’s risk across an portfolio of winners.

Piggybacking off Google Ventures, Google also operates a private equity fund (CapitalG) to invest in even later stage companies, including Lyft, Airbnb, Credit Karma, FanDuel and many many more.

This strategy of redeploying wealth into the ecosystem not only furthers tech and economic development worldwide, but ultimately creates a scenario where it is hard for Google to lose, regardless of Google’s fate as a company.

GoogleX

Moonshots are something only startups typically attempt. Google however flips the script, studying nearly impossible problems to try to create the transformative businesses of the future.

When pairing near infinite money with the brightest minds in the business, this can create huge returns. And startups/venture is a game of limited risk and unlimited upside.

For instance Waymo was a GoogleX spin out, which according to Morgan Stanley could be worth upwards of $70B by 2030. If the driverless market turns out as I see it, and Waymo is the one that wins, this is a massive undervaluation.

Considering Google only invested $1.1B in autonomous vehicles between 2009 and 2015, this would be a 70x ROI — a HUGE win.Other GoogleX projects include remote access wifi via balloons, autonomous drone delivery, Google Glass (ultimately an overhyped failure) and dozens of other projects, any of which could go big.

Nest & Google Home

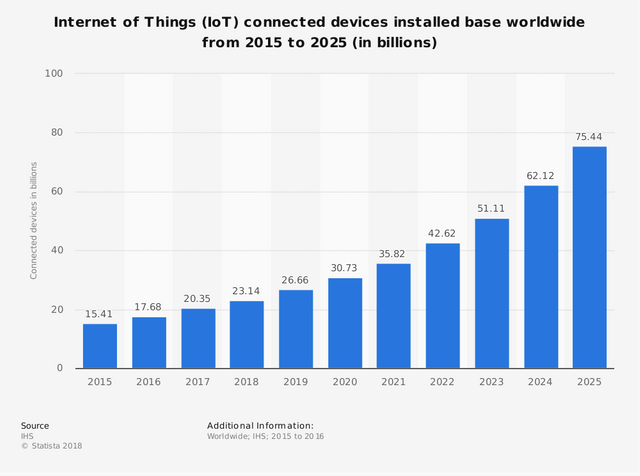

The internet of things is here to stay. Connected devices are coming online at an unprecedented pace — the IHS is forecasting 75B+ devices by 2025.

Google wants to be the at center of everything. And their progress in voice computing and machine learning has set the company up to do just that, though currently Amazon is well ahead.

The reason this battle is important is the hearts and minds of consumers. Attention and information is power, which translates to money.

And as home computing and connected devices become an increasingly large part of our everyday lives, the value of this space explodes. From both a data and an upsell perspective, the space is forecasted to grow 5x in the next 10 years.

And as the value of connected networks typically increases proportional to the square of its nodes, we could be looking at as much as a 25x increase in IoT market in the coming decade.

This combined with the absolute nature of voice (ie: there are no second and third search options — see issues with Google’s search business below), creates a true winner take all market where, assuming network effects associated with NLP (neuro linguisitc programming) and AI based speech recognition means that neither Amazon nor Google can afford to lose this race.

Google’s Greatest Challenges

Despite Google’s success, there are several big problems with the business. Alphabet’s ability to overcome these will dictate the success (or failure) of the Googly experiment.

NOTE: These are in no particular order.

1. Voice replacing search

“Ok Google, I don’t want to hear another ad”

Voice is a paradigm shift, especially for Google. And it is ironic. Google is the leader in voice and NLP, clearly outperforming competitors like Alexa, Cortana and Siri (a joke) in the fields of voice.

But that begs a bigger question: what happens to search results and paid ads without the screen interface? Will Google just read ads all day like Billy Mays? Or is there an ounce of integrity left?

That is the question. Currently Google overloads search results with shitty ads. But in voice, there is no page 2, page 3 or even #2. It is winner take all. You don’t want some device reading out a million options. You want the best option and you want it immediately.

So if voice disrupts Google core search business (61% of their overall revenue), the business fueling their driverless cars, their wifi balloons, Google Ventures and all of Alphabet’s interesting arms, how can the company survive?

2. Amazon doesn’t need Google ads

But Amazon no longer needs to advertise on Google. Amazon is organically outranking everything and has a massive customer base who consistently shop on Amazon.

That spells trouble for Google. Amazon accounts for a huge (yet ever dwindling) portion of Google’s revenue (in 2013 Amazon spent $157.7 million on Google ads, by 2016 their marketing spend was up to $7B — Sources: DigitalStrategyConsulting, BusinessInsider).

3. Weak leadership

Google’s too nice. The management team lacks the killer instincts needed to win.

Look at Facebook. Prior to 2012, Google OWNED online advertising. They let Zuckerberg and Sheryl Sandberg come in and steal their lunch. Facebook was valued around $50B in the summer of 2012, right after their IPO. Google could have (and should have) forced a hostile takeover.From then on Facebook stole ever larger shares of the digital advertising market. And then they acquired Instagram. How did Google let that happen?

And don’t even start on Amazon. Amazon USED to be one of Google’s biggest advertisers — until they didn’t need them anymore. Google let Amazon build an ecommerce monopoly (and search engine), effectively cutting Google out.

Google should have made a serious ecommerce play years ago. Instead Google recently partnered with Walmart.com — talk about a match made in hell. Both companies couldn’t care less about the other and realize the futility of working together but what option do they have? Google NEEDS an ecommerce play. And Walmart can’t figure out acquisition and growth against Amazon. Talk about two drowning men each pulling each other down.

4. Poor hardware performance

For years Google has been trying to diversify and add hardware as a core component of their business. It hasn’t been working.

Google sees Apple owning the customer and creating the world’s most valuable brand with basically just an iPhone and ask themselves, “why can’t we do that?”

Yet despite huge budgets and smart folks, most of their efforts have fallen flat (in terms of sales) and been seen as mainly me too products. Pixel phones, PixelBuds, Chromebooks… the vast majority have not been huge commercial successes. And let’s not forget Google Glass.

On a whole, Google has proved pretty ineffective in building, shipping and MARKETING hardware products.

5. Regulations + The Trump and Putin party

The last big threat Google’s currently facing comes from regulators. While the EU has already slammed Alphabet with a record $2.7B fine, there will be more in the pipeline. Combined with GDPR coming to Europe and the US realization that sites like Google and Facebook helped Russians influence the election, governments around the globe are starting the question the power of the internet companies.

While Google will almost certainly escape these unscathed due to mutually assured destruction (see this post), public sentiment is starting to turn against tech companies, hence why Google (and other tech companies) are starting to outpace Wall Street in lobbying.

Luckily Google has some gamechanging opportunities ahead of them (in no particular order).

Google’s Growth Opportunities

1. The OS for autonomous vehicles

We are racing towards a driverless world of transportation as a service. Google/Waymo is uniquely suited, especially considering their partnership with Lyft (among many other ride sharing providers) to dominate this market.

For a more detailed analysis on the societal and economic impacts of autonomy and how Google could replace their entire search advertising business, see this post.

In summary, autonomy will free 52 minutes per day for the American commuter. And as autonomy progresses the business opportunities and transformation of traditional space/real estate will represent trillions in uptapped value. Sleep your way into a new city, grab fast food (or a fine dining) at 80mph, plug into VR while driving cross country…

While it is impossible to predict the rate of adoption of autonomous vehicles due to regulatory concerns, no one is arguing the fact that this technology will change the world. There 1.2B cars worldwide. That is an ENORMOUS addressable market. Autonomy is interesting…

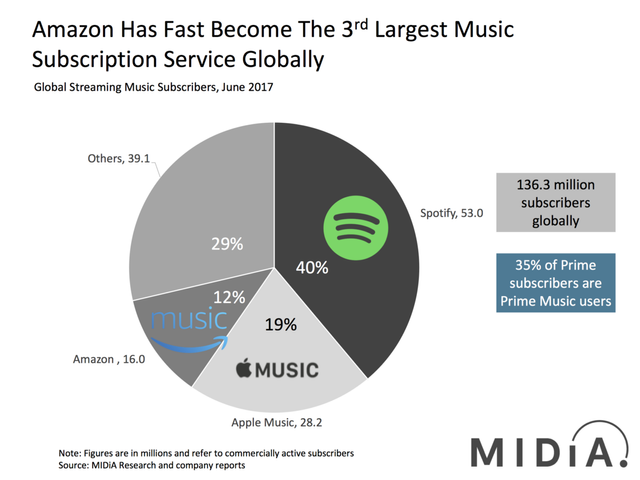

2. Expanding Google Play Music

It is surprising how little Google has done with paid content. Specifically, a low cost (or ad monetized) streaming music service could be hugely profitable. 80%+ phones worldwide are Android.

You would think Google could create an effective competitor to Spotify, Apple and Amazon. Yet they just haven’t. Spotify will be IPOing soon, with a valuation likely north of $19B. That isn’t chump change.

Seems like Google should get their act together.

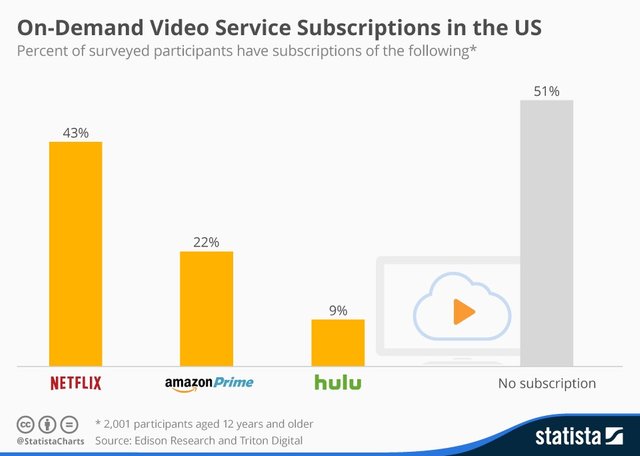

3. Expanding Youtube Red (Subscription Video)

Youtube is the 2nd largest search engine in the world and easily the largest video platform. And despite Google’s video dominance with 1B MAUs (monthly active users), Google is again getting killed — I am starting to sense a theme.

There is so much potential here. Netflix alone is valued at $94B. And the market for quality video content is constantly increasing. Content (and attention) is king, and video more than any other medium (short of VR), completely captures attention.

Netflix will spend $6–8B on original content in 2018. In 2017 they produced 1000 hours of original programming. And with shows like House of Cards, Orange is the New Black and Narcos, Netflix is nailing the content.

Even Amazon and Apple are betting big on original content, with $4.5B and $1B budgets respectively this year.

People pay for quality content. Subscription revenue trumps ad dollars everyday.4. Blockchain focused fund

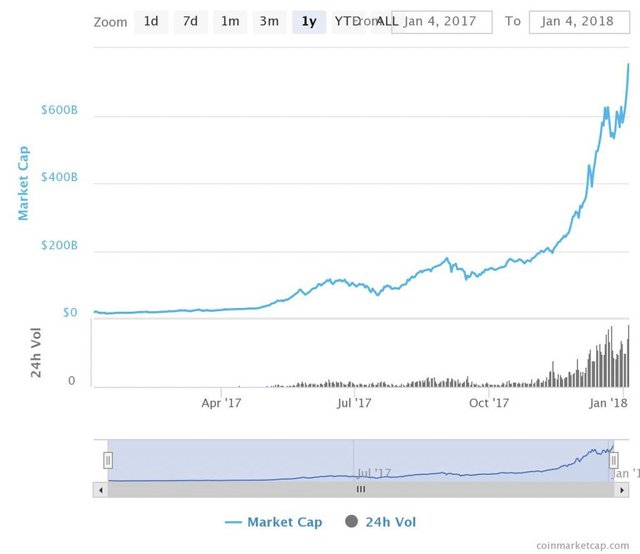

2017 has been the year of blockchain and ICOs. The crypto world has seen an explosion of decentralized furvor (and crazy speculation) where projects looking to (or at least promising to) create the internet of the future have raised MASSIVE sums of money to build large, decentralized networks.

Source: Bitcoin.com

Source: Bitcoin.com

And while much of the hype is just that, the potential of this technology is truly transformational and disruptive.

Although Google is one of the incumbents many crypto projects are looking to unseat, they have an interesting opportunity to play in the space.

If decentralized technology does in fact displace many of today’s centralized incumbents, it makes sense for Google to hedge their bets and invest in the most promising blockchain companies. Much like GV, Google’s venture capital arm, a long term crypto focused fund could set Google up with either potential partnerships or ownership of the industries of the future.

Acquisition Opportunities

Google has a huge war chest, it is time they do something with it. According to SiliconBeat, as of May 2016 Google had a whopping $73.1B in the bank(59% of that overseas).

Who should Alphabet acquire to set themselves up for future success? Here are some hints (in no particular order).

1. Ecommerce

Google gave the reins of the economy to Amazon, allowing Bezos to buy his way to monopoly.

Despite Amazon’s massive lead, accounting for 44% of US ecommerce sales in 2017 (Source: Recode), Google still needs a play here. And the Walmart.com partnership is a joke.

At this point it is probably impossible to beat Amazon at their own game. Instead of a single platform play, Google should build several niche verticals — specifically those Amazon struggles with. Three in particular with huge potential that currently outperform Amazon are: Etsy, Kickstarter (or Indiegogo) and Wayfair.

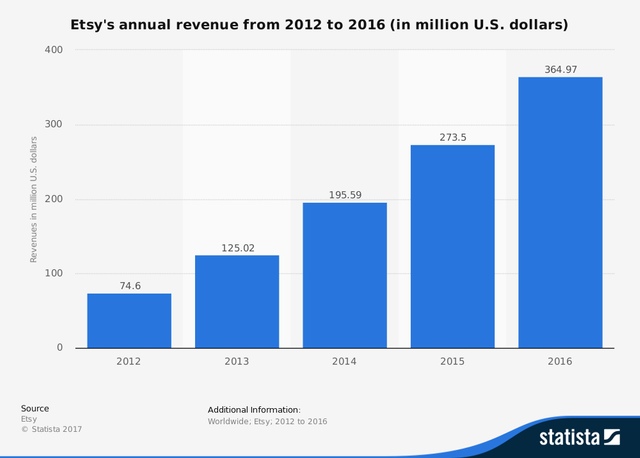

Etsy (market cap $2.38B) is an established, growing handmade craft and design marketplace with 1.9M active sellers, 31.7M active buyers and over 45M products on the site (Source: ExpandedRamblings). In contrast, Amazon is almost 100% manufactured products and thus a very different segment of the market for both buyers and sellers.

Kickstarter and Indiegogo are two of the biggest names in crowdfunding. And while finding valuations for each is challenging (Kickstarter is public benefits corporation and IGG has not made revenue numbers public), either one could likely be purchased for under a few billion. And owning the innovator’s platform creates plenty of opportunities, especially as the startups graduate to big boy business.

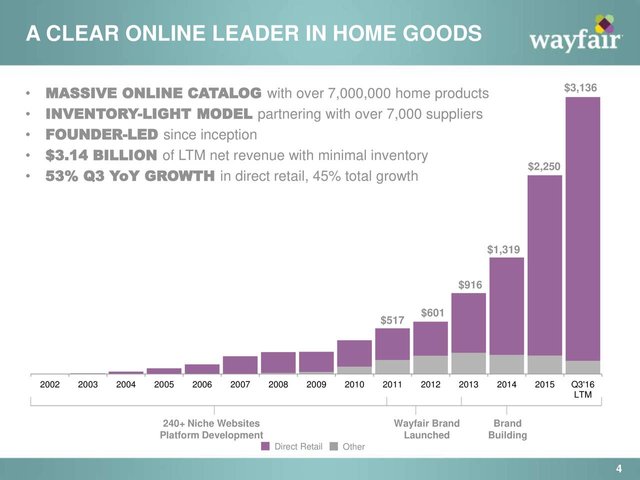

Wayfair (market cap $7.52B) is the last ecommerce company Google should acquire if they are serious about competing with Amazon. Wayfair is a massive furniture and home decor company (think IKEA online) with the last 12 months revenue exceeding $3.13B (as of Q3 2016).

The unfair advantage Wayfair has is in their furniture lines. I have seen Amazon struggle with furniture. The size, cost and logistics nightmare of shipping sofas and beds has made things hard for Bezos to build his everything store.

Source: Wayfair

Source: Wayfair

It helps that all three of these brands are based on the East Coast (NYC for the first two and Wayfair’s in Boston).This proximity allows for resource sharing and productive synergies across the organizations, especially with Etsy and Wayfair which have very similar target markets.

Combining this with Google’s ability to run free advertising for the platforms could help all three brands thrive and build large, defensible moats before Amazon had the chance to act.

As Google built up a portfolio of successful ecommerce companies, they could either acquire additional verticals or spinoff experienced teams to focus on other opportunities.

2. AR/VR Platform/Stack

There is a non-negligible chance that the next wave of internet is based around augmented and or virtual reality. For a company like Google at the cutting edge, they should focus on their OS approach in facilitating (and controlling) this transition.

In business, the true wealth accrues not to the first movers or to the businesses but the platforms. The company that builds the platforms, interfaces and mediums of exchange that facilitate augemented and virtual reality startups (and companies) will be the one that wins.

While plenty of companies are fighting to be the goggles of the future, this isn’t an exciting battle, or one Google can win (see issues with hardware). Instead Google should on building/acquiring the infrastructure and services needed to support this new wave of innovation — think the Youtube, the App Store or the AWS of AR/VR (likely with B2B and B2C facing platforms).

I am not qualified to assess the top players. Google however has the insight, expertise and distribution needed to make a turn a tiny platform into a mainstream leader.

Here are some potential candidates (specifically VR platforms), courtesy of ThinkMobiles. If I were Google, I’d look at Boost.VC portfolio companies.

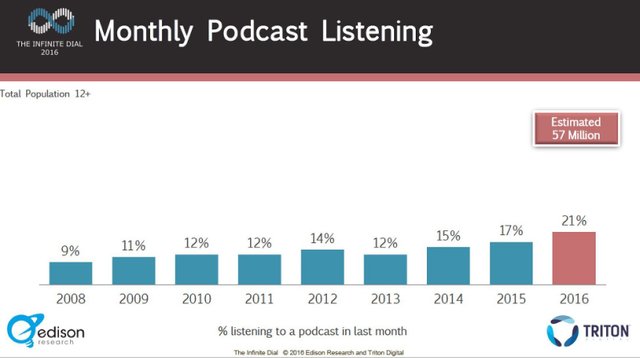

3. Podcasting

As host of The Syndicate podcast and a fan of numerous tech, VC and blockchain based shows, I’m bullish on podcasting. That said, the numbers speak for themselves.

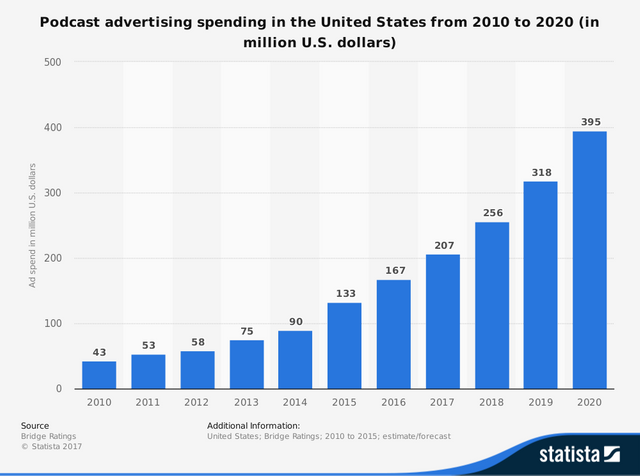

While not hugely lucrative (due to inefficiencies in the system), 21% of individuals over the age of 12 listened to a podcast in the last month — that’s 57M Americans (and growing rapidly). Attention and advertising dollars are starting to flood the space.

The biggest challenges today are the complexity of advertising and lack of analytics. Unlike most digital advertising, it is hard to setup and measure advertising. You don’t know where listeners drop off or if they even heard the ads. And finding/onboarding publishers is a one-off process requiring significant time investment.

There is no simple, easy to use system for buying and selling podcast ads.

This is something Google excels at, and should implement into their system. To effectively do this, Google needs to acquire verticalized ownership of both the podcast hosting companies and the podcasting apps.

In terms of podcasting hosting, outside of Amazon; Libsyn and Blubrry are the two largest hosting providers. Neither have publically disclosed venture funding and thus should be easy/cheap to acquire.

And on the consumer facing side, ownership of distribution/podcasting apps is key. To be on the safe side, Google should acquire each of the top 3–5 podcasting apps by number of downloads. For all future versions of Android, just make one of these the default podcasting app.

These 5–7 acquisitions shouldn’t cost more than several hundred million. And once Google owns the distribution, they can create a podcasting analytics platform and integrate podcasts into their advertising engine.

When that happens, more and more money will pour into podcast advertising for its targeted, longform engagement — likely leading to exponential revenue growth.

And since weekly podcast listeners listen to an average of 5 hours and 7 minutes of podcasts per week (Source: Salesforce), there is a huge amount of monetizable, high focused customer attention that Google could take easily advantage of.

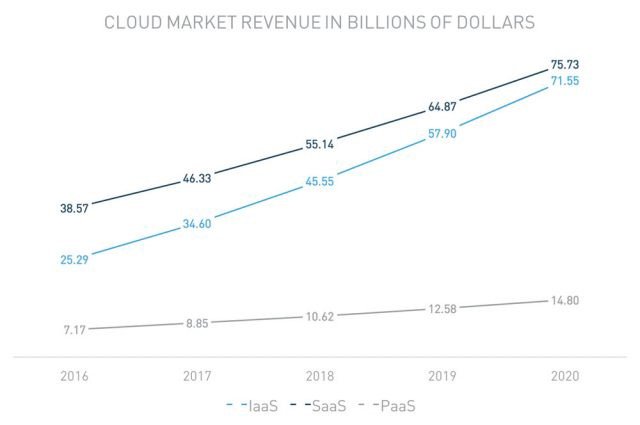

3. Enterprise Cloud Services

I’m not qualified to speak concerning who Google’s Enterprise Cloud Services division should buy, but considering the fact that they are being clobbered by Amazon and Microsoft, it seems logical that they need help.

As Infrastructure as a Service approaches a $75B market in 2020, Google’s pathetic sub-4% market share becomes a big concern for them.Here is more information from Goldman Sachs on the possible candidates.

4. Wild card 1— Ridesharing

We spoke previously about the possibilities of autonomous vehicles. While Google could work with existing providers, owning the entire operating system would prove significantly more profitable.

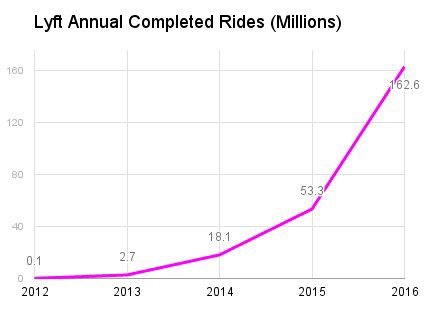

In this instance, acquiring Lyft could be a big bet on the company’s future. Lyft’s most recent funding round valued the company at $11B. While this is a sizeable sum, Lyft’s existing network effects and customer base are quite valueable.

Source: Forbes

With over 700k drivers, 1M+ rides per day and between 3–5M MAUs (monthly active users), Lyft is approaching 1/3 of the US ridesharing market. And while significantly less successful overseas, this acquisition would be a US play first and foremost.

Combining Google Maps to Lyft ride functionality and free search and in-app advertising for Lyft, Google could greatly help Lyft close the gap on Uber (especially thanks to Uber’s numerous transgressions).

But winning the ridesharing market isn’t the point, the point is autonomy (and upsells). For a more in-depth analysis, see this post.

The money isn’t in the fares, it is in the business around the experience. That could be Google’s big business of the future.

5. Wild card 2 — Telco

Imagine if Google owned Sprint. While easily the smallest of the US carriers, Sprint still has 50.4M customers. And Google owns Android. How hard would it be to offer Android users free services/switching bonuses? They could probably even use push notifications.

And if every Android phone came with a free two months of Sprint coverage, do you think many users would switch later on? I doubt it. Now in the US this is challenging due to the restrictive, long term contracts and upgrade costs. But with Google’s economic backing and ability to reach consumers, Sprint could switch to a more customer friendly monthly or yearly subscription model and still make great money.

And Google could add free Sprint advertising to search results.

“Best mobile carrier” — Sprint could show at the top of the ads results everytime, and be completely free.

While Sprint’s valued at $22.76B, this would be doable for Google. The impact on existing service providers would be huge. And because Google could better monetize via ads (even on iPhones), Sprint could charge lower fees and still make great money, causing users to switch to Sprint — greatly increasing the value of the acquisition, and crushing competitors in the process.

And of course Sprint would focus on selling Google’s hardware over Apple. This could Pixel poor sales performance with better in-store sales and focus and bundled discounts.

Plus as net neutrality dies (I hate it but at same time…), imagine the possibilities for an Google-Sprint supercompany. Zero rating will probably be the first (and hopefully only) impact of repealing net neutrality.

With a merger inplace, zero rating Youtube, Gmail and Google’s other properties would greatly increase traffic/usage from Sprint customers. And plenty of others would sign up Sprint for just this reason. Google is basically the internet for many people — zero rating would make it free.

The rating

Google is a once in a generation company and a driving force behind our world and economy today. As we race into a future full of paradigm shifts, the question for Alphabet’s leadership becomes how to extend their dominance and market leader status.

There are many challenges for Google in the coming years, but equally promising opportunities.

While I’d love to Google an A, I can’t . Given the inherent risks associated with their primary business and the upcoming paradigm shifts of voice and/or blockchain technology potentially disrupting their core, I am forced to give Alphabet a solid B+. While not quite as impressive as Amazon’s A, Google is easily one of the best businesses in history. (For more on Amazon, see this analysis).

If an A+ is a near infinitely defensible business, a B+ is all that bad.

Closing thoughts

Ten years from now, which tech giants will dominate the world? And how will humanity and society have “evolved” over this timeframe?

These are the big questions facing entrepreneurs and investors today. But with chaos comes opportunity, and the next 10 years will redefine the world as we know it (and likely the human species).

Will Google still be at the forefront? I don’t foresee Google making the acquisitions suggested above. Instead I see Google becoming the 2008 version of Microsoft, a shadow of its former self.

My money is on Amazon. Here’s why.

Learned something? Share this around on social to say “thanks!” and help others find this article.

And don't forget to subscribe if you haven't already!

Before you go…

If you got something actionable or valuable from this post, like this and share the article on Facebook and Twitter so your network can benefit from it too.

LIKE THIS ARTICLE? THEN YOU’LL REALLY WANT TO SIGN UP FOR MY NEWSLETTER OVER HERE — AND GET SOME FREE BONUSES!