The State of Stablecoins in 2018.

There are three main categories of stablecoins: fiat-collateralized, crypto-collateralized, and non-collateralized. In this blog post I shall attempt to review and go over each specific stablecoin projects.

1. Tether and TrustToken

By backing their tokens 1:1 with USD in the bank, these projects are super simple and are able to maintain the peg quite well. However, they will never work in the long-term for a variety of reasons. Firstly, it is against the ethos of decentralization to have the keys of a monetary system be held in 3 people's hands. This is even worse than governments, where power is completely monopolized by the creators of these projects, and creates perverse incentives which could harm the system. Secondly, this operation will never be able to scale. As the market capitalization for Tether and TrustToken gets larger, they will have to store more and more USD in banks. At a certain point (billions), it becomes impossible for banks to hold so much cash on their balance sheets, and Tether/TrustToken cannot grow beyond that. This means that Tether and TrustToken will only be effective in the short-term, if effective at all.

2. MakerDAO's Dai

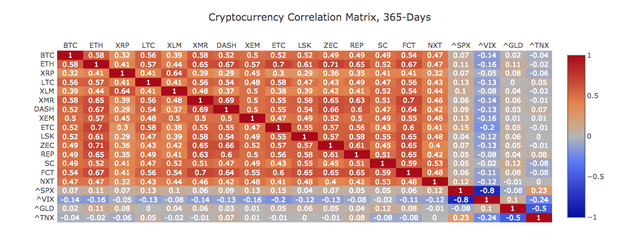

MakerDAO is an interesting, but fairly complex project which uses other cryptocurrencies as collateral for their stablecoin Dai. Aside from the fact that it is difficult for the layman to understand the MakerDAO system, it does have some fundamental flaws which are difficult to overcome. Firstly, because the Dai is collateralized by other cryptocurrencies, it is vulnerable to extrogenous factors, such as a sudden devaluation of the collateral. To overcome this, MakerDAO says that they will soon be able to collateralize their Dai with a basket of diversified, uncorrelated cryptocurrencies so that the likelihood of the entire collateral collapsing is low. Let us take a look at the correlations of cryptocurrencies:

Using data from here, it seems possible to build a fairly diversified portfolio of cryptocurrencies. However, this is severely misleading and is a misconception that MakerDAO has spread. Although 1-year correlations are fairly uncorrelated, all correlations go to 1 during a market crash. This means that it is, in fact, much more likely for the Dai's collateral to devalue severely with a crash of a single cryptocurrency like ETH or BTC.

Secondly, to accommodate for these market crashes, the Dai has to be over-collateralized. This means that there has to be more cryptocurrency in the system than circulating Dai, currently by 150%. Much like Tether and TrustToken, this creates an artificial cap on how big the Dai system can grow to. Today, for the market capitalization of Dai to be $10B, there must be at least $15B worth of ETH in the Maker collateral vault. That is currently almost 30% of the current ETH supply! This is an inefficient use of capital, but it is the cost of creating a buffer for possible devaluations of the collateral.

Lastly, any collateralized currency, like the Dai, is not particularly interesting from a money perspective. The Dai is unable to become an independent monetary system that can stand on its own legs without relying on other assets. Because of the way collateral works in the Dai system, the Dai economy can really never grow to anything larger than a small % of the crypto-economy.

3. Basecoin, Fragments, Carbon Money

These projects are non-collateralized stablecoins, which solves my issues with MakerDAO and Tether. However, they too, have their own kind of problems.

Although it is unfair to consider these three projects as homogenous, they operate under the same premise: expand and contract the money supply to control price, as stated in the Quantity Theory of Money. When the coin is trading above $1.00, print new coins and distribute them out. Conversely, when the coin is trading below $1.00, contract the money supply by destroying some coins — this is done through schemes such as Base Bonds, Fragment Bonds or Carbon Credits. The theory is that when you increase the money supply, this newly minted coins will get auctioned off into the free market and create downward price pressure. When you contract the money supply, each circulating coin is more scarce, and this should in theory bid up the price.

I believe that this model of stability is fundamentally flawed — there are many issues with religiously following the Quantity Theory of Money. The theory may hold true in the long-run, but there is no concrete evidence that it applies in the short-run as well. This is an example of how fragile the system is in the short-run: when the demand for Basecoin increases, people are willing to buy the coin above par value, let's say at $1.05. To push the price back down, the Basecoin 'algorithmic central bank' prints 10,000 new Basecoins and distributes it to the bond holders and the share holders. When the bond holders and share holders sell off these coins, the desired downward price pressure will be produced. But what happens when these bond and shareholders just hoard these newly minted coins instead of selling them? When there is no selling, prices will not change. Hence, the system sees that price is still not going down and algorithmically decides to increase the supply even more. All this while, the bond holders and share holders continue to sit still, pocketing all the newly created supply while the price still does not go down.

This scenario can happen in the short-run because the system is reliant on humans to actively sell off the newly created supply. There will always be a lag between changes in supply and correction of price, making the system less robust and reactive to price fluctuations. This also holds true for monetary contractions, but even worse. First, it takes time for people to actually buy up these bonds. Once they do, the money supply is effectively contracted. However, as before, the price of the coin does not magically get pushed back up to par value by adjusting the supply. The system still requires people to buy up these coins — and if there is a negative outlook on the future of the system, no one will.

The problem with a system that relies on macroeconomic theory is that there are no guarantees that it would work at all in the short-run. There are many variations of the expansion and contraction of the money supply, but they all suffer from the same fate in that they will likely break in the short-run. Steps to overcome this include back-up plans like a Reserve or a Bond-fund, but that too can be broken or drained relatively simply. Ideally, there must exist a stablecoin solution that is able to instantly adjust price back to par value and provide some sort of provable guarantees of price-stability. Such a stablecoin will be exponentially more robust and resilient than Basecoin, Fragments, and Carbon.

Concluding Thoughts

An examination of the existing stablecoin projects in early 2018 indicate that there is still a long way to go to build a new type of money. It is clear that any collateralized stablecoin will not be able to scale and suffers problems of custody and insolvency. To solve these problems, we must create an independent monetary system like Basecoin, but with a better and simpler model of stability. The Quantity Theory of Money does not hold true in the short-run and stablecoin systems which adopt this model can easily fall into an irrecoverable death spiral.

Stablecoins are much larger and more significant than just enabling specific financial contracts or for traders to trade — it is the next step for the evolution of money. This new money will be algorithmically controlled, free of political bearings and serve its use as the most advanced medium of exchange and unit of account we have in human history. So we must get it right.

In the later parts of his life, John Nash wrote and spoke about the possibility of an "ideal money". This would be a global money standard which would have value similar to that of standard measures, like the metric system. Of course, creating such a standard is virtually impossible from a political standpoint.

Cryptocurrencies have provided us with a way to create a decentralized currency — what is left to solve is price-stability.

Thank You

Trade on Binance. Where the fees are only 0.05%.

If this blog post has entertained or helped you to profit, please follow, upvote, resteem and/or consider buying me a beer:

Cool, following you. Whats your current favorite coin/token?