Learn Python Series (#32) - Data Science Part 3 - Pandas

Learn Python Series (#32) - Data Science Part 3 - Pandas

![]()

Repository

What will I learn?

- You will learn what "time series resampling" means;

- how and why resampling provides essential insights looking at different time series windows / resolutions;

- how to aggregate multiple columns of data and use column-specific resampling rules;

- how to compute rolling (moving) window values.

Requirements

- A working modern computer running macOS, Windows or Ubuntu;

- An installed Python 3(.7) distribution, such as (for example) the Anaconda Distribution;

- The ambition to learn Python programming.

Difficulty

- Beginner, intermediate

Additional sample code files

The full - and working! - iPython tutorial sample code file is included for you to download and run for yourself right here:

The example CSV file that was used in the #31 episodes is copied to the lps-032 folder as well:

GitHub Account

Learn Python Series (#32) - Data Science Part 3 - Pandas

Re-loading the actual BTCUSDT financial data using pandas

First, let's again read and open the file btcusdt_20190602_20190604_1min_hloc.csv found here on my GitHub account, (after having saved the file to your current working directory, from which you're also opening it using .read_csv()):

import pandas as pd

df = pd.read_csv('btcusdt_20190602_20190604_1min_hloc.csv',

parse_dates=['datetime'], index_col='datetime')

df.head()

| open | high | low | close | volume | |

|---|---|---|---|---|---|

| datetime | |||||

| 2019-06-02 00:00:00+00:00 | 8545.10 | 8548.55 | 8535.98 | 8537.67 | 17.349543 |

| 2019-06-02 00:01:00+00:00 | 8537.53 | 8543.49 | 8524.00 | 8534.66 | 31.599922 |

| 2019-06-02 00:02:00+00:00 | 8533.64 | 8540.13 | 8529.98 | 8534.97 | 7.011458 |

| 2019-06-02 00:03:00+00:00 | 8534.97 | 8551.76 | 8534.00 | 8551.76 | 5.992965 |

| 2019-06-02 00:04:00+00:00 | 8551.76 | 8554.76 | 8544.62 | 8549.30 | 15.771411 |

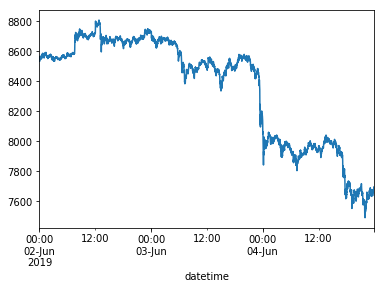

Let's again plot the opening prices of Bitcoin per minute, for a visual reference (to be compared shortly hereafter in the remainder of this tutorial episode):

%matplotlib inline

df['open'].plot()

<matplotlib.axes._subplots.AxesSubplot at 0x1182a3860>

Resampling time series using .resample()

A very interesting features the pandas library provides, is time series resampling. In essence this means grouping a number of small time span data rows into a larger time span.

For example, if you "resample" the current DataFrame consisting of 1-minute Binance ticks on the BTC_USDT trading pair into hourly intervals, that means you are grouping 60 1-minute ticks into 1 hourly tick.

To do this, you can use the .resample() method and pass in a so-called time span "offset alias" (= frequency) as the method argument.

For example, to resample the "open" column values (the BTCUSDT opening price data), using the mean values, and to assign those values to a new df_hourly DataFrame:

df_hourly = df['open'].resample('H').mean()

df_hourly.head()

datetime

2019-06-02 00:00:00+00:00 8562.740500

2019-06-02 01:00:00+00:00 8570.234667

2019-06-02 02:00:00+00:00 8565.278167

2019-06-02 03:00:00+00:00 8551.818333

2019-06-02 04:00:00+00:00 8553.886333

Freq: H, Name: open, dtype: float64

As you can see in the above .head() output, indeed the 1 minute ticks are precisely grouped into hourly values now.

It is also possible to achieve the same DataFrame output, by grouping by 60 minutes. This might seem trivial / just another way to achieve the same effect, but please note that it is also possible to prepend an integer value as a multiplier to the time span offset aliases (e.g. "5min", "15min", "60min", "4H", et cetera):

df_60min = df['open'].resample('60min').mean()

df_60min.head()

datetime

2019-06-02 00:00:00+00:00 8562.740500

2019-06-02 01:00:00+00:00 8570.234667

2019-06-02 02:00:00+00:00 8565.278167

2019-06-02 03:00:00+00:00 8551.818333

2019-06-02 04:00:00+00:00 8553.886333

Freq: 60T, Name: open, dtype: float64

Resampling time series data by aggregating (using .agg()) multiple columns each with a different operation

In the previous examples it was explained how to resample one column of data values (the 1-minute opening prices of BTCUSDT) into larger time spans. However, our current data set contains multiple columns of data ("open", "low", "high", "close", "volume") and ideally you want to resample each column differently.

For example:

- the "opening prices" of 1-hour ticks should stay the first value of the first minute of data. Each hour of data still began with the first tick of data;

- the "low prices" within 1 hour of data should be the minimum value recorded within that entire hour;

- the "high prices" within 1 hour of data should be the maximum value recorded within that entire hour;

- the "closing prices" should remain the last recorded value;

- the "volume" data should be summed as a cumulative value within each hour.

To do this, you can resample by chaining the .resample() method with an agg() (short for "aggregate") method, and then pass in a dictionary containing key-value pairs reflected by "column": "how"). Like so:

df_complete_1h = df.resample('H').agg({

'open': 'first',

'high': 'max',

'low': 'min',

'close': 'max',

'volume': 'sum'

})

df_complete_1h.head()

| open | high | low | close | volume | |

|---|---|---|---|---|---|

| datetime | |||||

| 2019-06-02 00:00:00+00:00 | 8545.10 | 8588.33 | 8524.00 | 8585.88 | 593.133892 |

| 2019-06-02 01:00:00+00:00 | 8564.97 | 8598.00 | 8550.89 | 8595.58 | 787.293606 |

| 2019-06-02 02:00:00+00:00 | 8570.35 | 8582.64 | 8540.00 | 8582.15 | 660.086969 |

| 2019-06-02 03:00:00+00:00 | 8549.23 | 8569.23 | 8525.97 | 8565.81 | 664.017888 |

| 2019-06-02 04:00:00+00:00 | 8545.93 | 8573.18 | 8540.40 | 8570.53 | 498.116310 |

Why multi-dimensional data-specific resampling and aggregation is very powerful and useful:

The techniques discussed just now are very powerful and useful, because - in case you (for example) want to perform technical analysis on OHLC&Volume data ticks on multiple time span resolutions / intervals -, when taking a close look at trading data (for example on an exchange such as Binance, or using visual charts provided via TradingView charting widgets), and "zooming in" on the 1-minute candles, price might appear to be in a short-term downtrend, but when zooming out to (for example) the 4H time span resolution then you suddenly notice price is still in an uptrend.

Visually inspecting time series (e.g. trading) data using just one specific time span resolution can therefore be deceiving and could lead you to forming the wrong conclusions (which can be very costly); when in a major (large time span) uptrend but focusing only on 1-minute (small time span) data, merely correcting in a short-term downtrend, you might be inclined to sell, only very shortly afterwards finding out the major (large time span) uptrend to continue. And vice versa, of course. Deriving insights by looking at "multiple time series zoom levels", is very important to be able to properly estimate the "intensity" of "change" and "direction".

Using the combined resample() and agg() data grouping methods, as explained above, the only data you need to fetch from source is the smallest time span resolution you are interested in. On Binance for example you can view the time span resolutions "1min", "3min", "5min", "15min", "30min", "1H", "2H", "4H", "6H", "12H", "1D", "1W" and "1M".

By fetching only the 1-min k-line tick data, you can resample and aggregate all time span resolution data, which can bring you better insights to come to better decision making: exactly the core objective of Data Science.

Rolling window calculations using .rolling()

Both in Data Science (in general) and financial technical analysis (specifically), keeping track of rolling / moving averages may yield powerful new insights. When you're active with crypto currencies, at some point (rather sooner than later, probably) you will come accross exchanges for trading tokens, which come with a multitude of "technical indicators". Again looking at the Binance exchange, in this example case at the BTCUSDT trading pair (Bitcoin against the USD-pegged Tether token), by default (viewing any time span resolution) in the same charts where the Open-Low-High-Close candles are plotted you'll also see two colored lines dubbed as "MA(25)" and "MA(99)".

In more financially versed circles, those two "technical indicators" are referred to as "Simple Moving Averages" (as opposed to for example "Exponential Moving Averages").

A Simple Moving Average is computed by looking (at any given tick) at N interval ticks backward in time, then computing the mean (average) value of those N ticks, and adding that SMA value to the current tick.

For example "(S)MA(25)" on Binance means: "let's use the previous 25 minute values, compute the mean value from those, and use that as a new value; the next minute we will shift upward 1 tick and re-compute the mean values for the next interval". In this case (at "MA(25)") N=25 and the "MA(99)" indicators uses N=99.

The mean values are "moving" or "rolling" as time goes by, and by storing those rolling averages as a new column in our DataFrame we get a much "smoother" representation of how price has been developing over time.

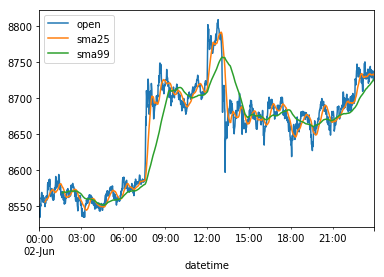

pandas provides a .rolling() method to compute the same data you see on a trading exchange such as Binance. In order to produce similar results, let's again use the original DataFrame (the non-resampled 1-minute ticks found in the provided CSV file), but this time only the 'open' price column data.

import pandas as pd

df = pd.read_csv('btcusdt_20190602_20190604_1min_hloc.csv',

parse_dates=['datetime'], index_col='datetime')

df['sma25'] = df['open'].rolling(window=25).mean()

df['sma99'] = df['open'].rolling(window=99).mean()

df[['open','sma25','sma99']].tail()

| open | sma25 | sma99 | |

|---|---|---|---|

| datetime | |||

| 2019-06-04 23:55:00+00:00 | 7676.54 | 7659.2484 | 7645.560404 |

| 2019-06-04 23:56:00+00:00 | 7689.76 | 7660.5348 | 7646.478081 |

| 2019-06-04 23:57:00+00:00 | 7696.69 | 7662.3408 | 7647.454747 |

| 2019-06-04 23:58:00+00:00 | 7697.66 | 7664.1404 | 7648.441212 |

| 2019-06-04 23:59:00+00:00 | 7690.97 | 7665.6016 | 7649.447677 |

The code line ...

df['sma25'] = df['open'].rolling(window=25).mean()

... means:

- let's create a new DataFrame column named "sma25";

- use a vectorised / column-based operation method on every row (cell) within that DataFrame column;

- by using the data found in the "open" column;

- use N=25 as the rolling window;

- and compute & store its mean (average) value in the "sma25" column.

If we now plot the 1-minute data ticks found in columns 'open','sma25' and 'sma99', and for visualisation matters let's only plot the 1-minute ticks of June, 2, 2019 - otherwise the lines would be too close to visually distinguish -, we get the following visual overview:

%matplotlib inline

df[['open','sma25','sma99']]['2019-06-02'].plot()

<matplotlib.axes._subplots.AxesSubplot at 0x1193bc3c8>

Nota bene: on the "sma99" data, since we need 99 ticks of data before we're able to begin plotting, if you take a close look at the above plot, bottom-left, on the green sma99 line, you see that there's a "gap".

The same can be found when printing the first 5 values using .head() (instead of .tail()):

df[['open','sma25','sma99']].head()

| open | sma25 | sma99 | |

|---|---|---|---|

| datetime | |||

| 2019-06-02 00:00:00+00:00 | 8545.10 | NaN | NaN |

| 2019-06-02 00:01:00+00:00 | 8537.53 | NaN | NaN |

| 2019-06-02 00:02:00+00:00 | 8533.64 | NaN | NaN |

| 2019-06-02 00:03:00+00:00 | 8534.97 | NaN | NaN |

| 2019-06-02 00:04:00+00:00 | 8551.76 | NaN | NaN |

The NaN values mean "Not a Number" (PS: in a forthcoming Data Science episode using pandas you'll learn about multiple ways on dealing with missing data, and dealing with "malformed" or even "incorrect" data points, and how to deal with those in a process called "Data Munging").

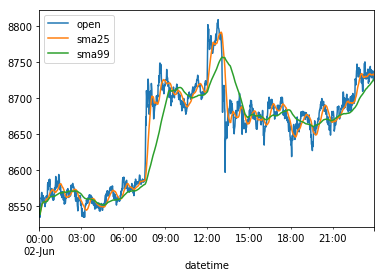

The .rolling() method comes with a parameter called min_periods=, which is by default set to the same number N as the window= parameter, in this case 25 and 99, respectively.

However, if we explicitly pass min_periods=0, then immeditely a "best-guess" value is computed based on < N values (meaning, at the first tick, the "sma25" value is identical to the "open" value, on the second tick "sma25" is the mean value of current and the previous ticks, until equal to or more than N ticks are present).

In code:

df['sma25'] = df['open'].rolling(window=25, min_periods=0).mean()

df['sma99'] = df['open'].rolling(window=99, min_periods=0).mean()

df[['open','sma25','sma99']].head()

| open | sma25 | sma99 | |

|---|---|---|---|

| datetime | |||

| 2019-06-02 00:00:00+00:00 | 8545.10 | 8545.100000 | 8545.100000 |

| 2019-06-02 00:01:00+00:00 | 8537.53 | 8541.315000 | 8541.315000 |

| 2019-06-02 00:02:00+00:00 | 8533.64 | 8538.756667 | 8538.756667 |

| 2019-06-02 00:03:00+00:00 | 8534.97 | 8537.810000 | 8537.810000 |

| 2019-06-02 00:04:00+00:00 | 8551.76 | 8540.600000 | 8540.600000 |

Visually plotted:

%matplotlib inline

df[['open','sma25','sma99']]['2019-06-02'].plot()

<matplotlib.axes._subplots.AxesSubplot at 0x106218a20>

And indeed, as you can see (while looking closely at the plot data bottom-left) now there's no missing gap, as there are no NaN values in the "sma25" and "sma99" columns.

What did we learn, hopefully?

Apart from how to (technically) use the pandas methods .resample(), .agg() and .rolling(), hopefully you've also learned why using those techniques provide essential insights while analysing time series data, such as crypto currency trading data.

Thank you for your time!

Curriculum (of the Learn Python Series):

- Learn Python Series - Intro

- Learn Python Series (#2) - Handling Strings Part 1

- Learn Python Series (#3) - Handling Strings Part 2

- Learn Python Series (#4) - Round-Up #1

- Learn Python Series (#5) - Handling Lists Part 1

- Learn Python Series (#6) - Handling Lists Part 2

- Learn Python Series (#7) - Handling Dictionaries

- Learn Python Series (#8) - Handling Tuples

- Learn Python Series (#9) - Using Import

- Learn Python Series (#10) - Matplotlib Part 1

- Learn Python Series (#11) - NumPy Part 1

- Learn Python Series (#12) - Handling Files

- Learn Python Series (#13) - Mini Project - Developing a Web Crawler Part 1

- Learn Python Series (#14) - Mini Project - Developing a Web Crawler Part 2

- Learn Python Series (#15) - Handling JSON

- Learn Python Series (#16) - Mini Project - Developing a Web Crawler Part 3

- Learn Python Series (#17) - Roundup #2 - Combining and analyzing any-to-any multi-currency historical data

- Learn Python Series (#18) - PyMongo Part 1

- Learn Python Series (#19) - PyMongo Part 2

- Learn Python Series (#20) - PyMongo Part 3

- Learn Python Series (#21) - Handling Dates and Time Part 1

- Learn Python Series (#22) - Handling Dates and Time Part 2

- Learn Python Series (#23) - Handling Regular Expressions Part 1

- Learn Python Series (#24) - Handling Regular Expressions Part 2

- Learn Python Series (#25) - Handling Regular Expressions Part 3

- Learn Python Series (#26) - pipenv & Visual Studio Code

- Learn Python Series (#27) - Handling Strings Part 3 (F-Strings)

- Learn Python Series (#28) - Using Pickle and Shelve

- Learn Python Series (#29) - Handling CSV

- Learn Python Series (#30) - Data Science Part 1 - Pandas

- Learn Python Series (#31) - Data Science Part 2 - Pandas

Thank you for your contribution @scipio.

After reviewing your tutorial we suggest the following points listed below:

Use shorter paragraphs and give breaks between them. It will make it easier to read your tutorial.

Improve the structure of the tutorial.

Thank you for following some suggestions we gave in your previous tutorial.

Looking forward to your upcoming tutorials.

Your contribution has been evaluated according to Utopian policies and guidelines, as well as a predefined set of questions pertaining to the category.

To view those questions and the relevant answers related to your post, click here.

Need help? Chat with us on Discord.

[utopian-moderator]

Thank you for your review, @portugalcoin! Keep up the good work!

Thank you scipio! You've just received an upvote of 33% by artturtle!

Learn how I will upvote each and every one of your posts

Please come visit me to see my daily report detailing my current upvote power and how much I'm currently upvoting.

Hi @scipio!

Your post was upvoted by @steem-ua, new Steem dApp, using UserAuthority for algorithmic post curation!

Your post is eligible for our upvote, thanks to our collaboration with @utopian-io!

Feel free to join our @steem-ua Discord server

Hey, @scipio!

Thanks for contributing on Utopian.

We’re already looking forward to your next contribution!

Get higher incentives and support Utopian.io!

Simply set @utopian.pay as a 5% (or higher) payout beneficiary on your contribution post (via SteemPlus or Steeditor).

Want to chat? Join us on Discord https://discord.gg/h52nFrV.

Vote for Utopian Witness!

Thanks for taking the time to thoroughly (and accurately) elaborate on my two questions. This certainly helped bring clarification to the subject for me What is Python Used for (https://light-it.net/blog/top-three-industries-that-use-python-for-big-data-projects/) Reflecting what others have said, I think this could be helpful to many readers on this subreddit. If any questions come to mind over what you wrote, I'll send them your way.